- Your cart is empty

- Continue Shopping

R Factor

R Factor

for MetaTrader 4 in MetaTra")

$30.99

-97%Add to cart

Buy Now

Product Description

R FACTOR Expert Advisor with Proprietary Dynamic Portfolio Management System

Rfactor + Set files

ALL old version + V1.925 + presets

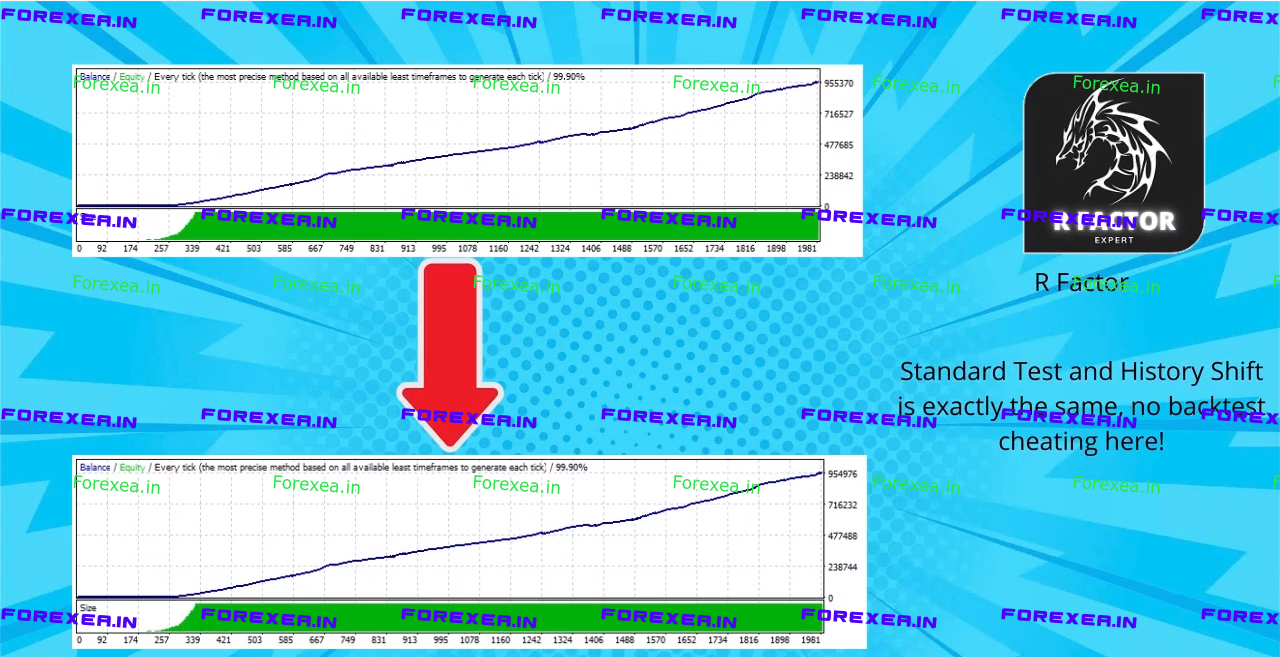

After 4 years of development and almost 3 years of real positive results, we are finally confident in sharing our strategy with the MQL5 community. It has always been important for us that the strategy performed positively for the creator before it could be shared. Skin In The Game is essential to demonstrate the belief in the strategy and also to provide a continuous improvement of it.

Anyone who has been in this market for some time has certainly been there: You develop or acquire a strategy, which has been extensively tested, using methods of robustness, randomness, Walk Forward Analysis, etc., but right when it is applied to your account real it begins to face a difficult period, a long drawdown, a market for which it was not prepared. This may not mean that the strategy has stopped working, only that the market is in a difficult cycle for the strategy at the moment, however it affects the psychological of any person, as the different cycles of the market can last for months or more and it is difficult for anyone endure these long periods of loss. And meanwhile, another strategy or asset that is not part of your portfolio, ends up performing very well, leaving your psychological even more hurt for having chosen the wrong strategy for the moment.

So assuming that the market works in cycles and certain assets can perform better or worse than others during these cycles, we developed a simple and very effective strategy for markets in times of congestion, and we applied a proprietary dynamic portfolio balancing algorithm, inspired by Kelly Criterion management, which automatically adds more weight to the winning pairs, while lessening the impact of losses by losing pairs in the period.

Therefore, according to the developed R Factor algorithm, the winning pairs grow in the portfolio independently, pulling more weight and responsibility over the global portfolio, thus increasing the potential current and future gains, while the losing pairs have their significance and impact on profits reduced. This of course tends to increase the volatility of the portfolio, however the potential profit that is achieved makes the equation much more favorable to take greater risks and consequently greater gains.

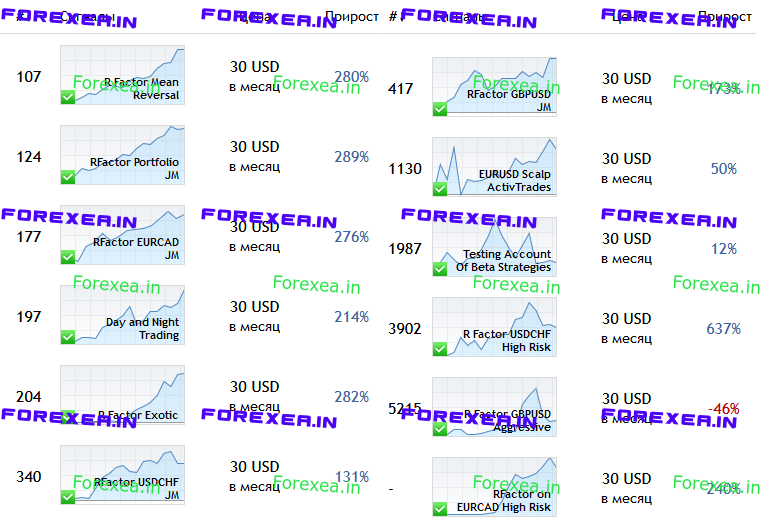

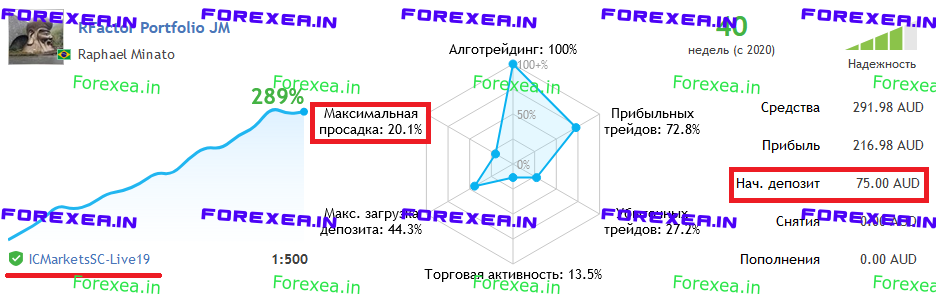

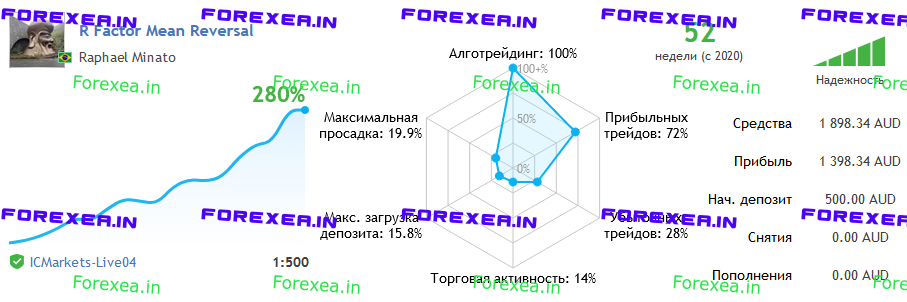

Below are some signal links of the performance in real account of several sets of R Factor, some with almost 3 years of recorded performance. It is important to say that a good past performance does not guarantee a good future result, however it is a positive indication that the strategy can support many different scenarios and with good chances of adapting to the constant changes of the market.

https://www.mql5.com/pt/signals/734515

https://www.mql5.com/pt/signals/743734

https://www.mql5.com/pt/signals/530561

To achieve a great performance, we highly recommend the use of brokers with an ECN account with low spreads and fair commission.

Top Characteristics of the Strategy:

– Defined Stop Loss and Dynamic Take Profit on all trades

– Just One trade per pair at a time. No Averaging, No Martingale.

– Dynamically portfolio balance proprietary algorithm that changes the weight and responsibility of each pair

– Intelligent Trade Exit System

– Almost 3 years live proved algorithm

– Proprietary Backtest Simulation of High Spread periods

– Low starting capital required (starting at 30 USD for one pair or 100 USD for the complete portfolio w/ 13 pairs)

Exclusive Telegram Group For R Factor customers that purchase the full version – Contact us with your proof of purchase of the full version to join and stay updated with the latest developments, strategies and new sets.

1 review for R Factor

Related products

-97%

Gegatrade Pro

$12.99

-97%

AlgoScalpPro

$18.99

-100%

Detroit Trade V2.2

$8.99

-97%Featured

Numenwave

$8.19

-95%

Capital Trade EA

$28.99

-69%

CAP Zone Recovery EA PRO

$21.99

-79%

Take a Break + Indicator

$20.99

-85%

Cap Asian Scalper

$8.99

admin –

The Best!